1) Executive Summary

Indiaʼs transition to electric mobility has entered a decisive phase. The national ambition targets a 30% EV penetration by 2030. Yet, EVs accounted for only ~8% of new vehicle sales in 2025, indicating that incremental progress will not be sufficient to meet climate, air-quality, and energy-security objectives. The next phase of growth must therefore prioritise segments where electrification is already economically and operationally viable. (NITI Aayog, 2025)

One such segment is last-mile delivery.

Urban last-mile logistics, powered predominantly by two-wheelers and three-wheelers, sits at the intersection of high vehicle utilisation, short trip lengths, and dense population exposure. It is simultaneously one of the most emissions-intensive components of urban transport and one of the most technically ready for electrification.

This whitepaper combines:

• Primary insights from a survey of over 6,000 delivery partners (Flipkart wishmasters) operating across urban India, and

• Secondary analysis from national policy, fiscal, and industry research

to answer a central question:

What will it take to electrify last-mile delivery fleets at scale, and what barriers need to be removed?

This is what our study revealed:

• Readiness is high: Over 45% of delivery partners express willingness to adopt EVs.

• Routes are compatible: Most daily travel falls within 40–80 km, well within current electric two-wheeler capabilities.

• The adoption gap is structural, not behavioural: High upfront costs, uneven charging access, technology trust, and lifecycle uncertainty dominate decision-making.

These ground-level insights closely mirror national diagnostics that identify financing risk, charging viability, awareness gaps, and data fragmentation as the primary barriers to EV adoption in India.

From a climate and fiscal perspective, last-mile electrification is also one of the most efficient uses of public and private capital. Evidence shows that electric two-wheelers deliver significantly higher CO₂ abatement per rupee of incentive than electric passenger cars, making them a high-impact priority for the coming decade. (CSEP, 2026)

This paper demonstrates that scaling last-mile electrification requires a deliberately designed ecosystem and not through isolated actions. Electrification succeeds only when financing, charging, vehicle design, workforce capability, and lifecycle assurance are developed as a single, coordinated system. By reducing operational risk and improving predictability for delivery partners, ecosystem design transforms EV adoption from a high-risk capital decision into a viable, everyday operating choice - enabling scale, inclusion, and sustained impact.

If aligned, last-mile delivery can become Indiaʼs fastest and most visible pathway to electric mobility at scale.

Industry Perspective

Divya Sharma, Executive Director - India, Climate Group

Across global markets, experience shows that electric mobility transitions accelerate when high-utilisation fleet segments move first. These fleets create predictable demand, enable charging infrastructure, and demonstrate that electrification works not only technically, but also economically.

Urban last-mile delivery sits squarely in this category. Its high utilisation and predictable routes make it one of the most effective levers for rapid transport decarbonisation, while delivering additional benefits such as improved urban air quality and more resilient logistics systems. With Indiaʼs rapidly expanding e-commerce sector, delivery networks are scaling quickly, making this segment an important opportunity to accelerate the electrification.

Scaling adoption requires ecosystem alignment - affordable financing, accessible charging, and vehicles suited to real-world delivery operations. Understanding the experiences and needs of delivery partners is therefore critical to identifying what works today and what is needed to accelerate EV adoption. With the right enabling environment, India can advance its 2030 transport electrification goals while building an inclusive electric mobility ecosystem.

2) Why the Last Mile Matters

Urban logistics is undergoing rapid transformation in India, driven by sustained growth in e-commerce, food delivery, and quick-commerce platforms. This growth has led to a sharp increase in short-distance, high-frequency delivery trips concentrated in dense urban areas.

Globally, research indicates that up to 50% of logistics-related emissions occur in the final delivery leg, despite it being the shortest component of the supply chain. In India, this impact is magnified by the continued reliance on petrol-powered two-wheelers for last-mile delivery, resulting in elevated emissions of PM2.5, NOx, and CO₂ in densely populated neighborhoods (CII & Clean Air Fund, 2025).

• Approximately 75% of Indiaʼs vehicle fleet consists of two-wheelers, making this segment central to any transport decarbonisation strategy (NITI Aayog, 2025)

• Urban travel distances are relatively short, with the majority of trips under 10 km, aligning well with EV range capabilities (NITI Aayog, 2025).

• Delivery vehicles are high-utilisation assets, often travelling more kilometres per day than personal vehicles, amplifying both fuel savings and emissions reductions per vehicle (CII & Clean Air Fund, 2025).

Together, these factors position last-mile delivery as one of the most electrification-ready segments of Indiaʼs transport ecosystem.

3) What Delivery Partners Tell Us

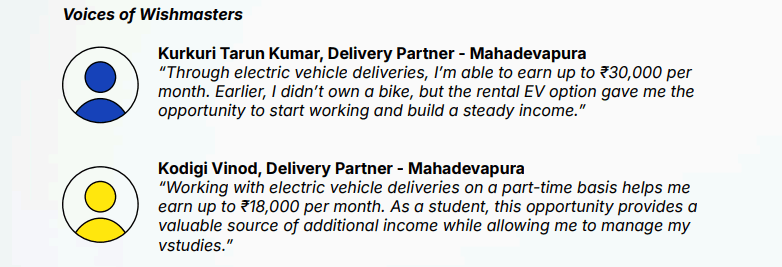

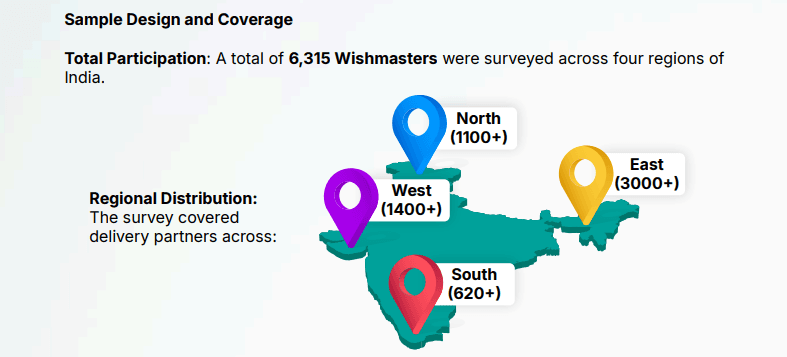

Insights from a structured survey of over 6,000 active delivery partners (Flipkart Wishmasters) across Tier 1 and Tier 2 cities provide a ground-level view of EV readiness.

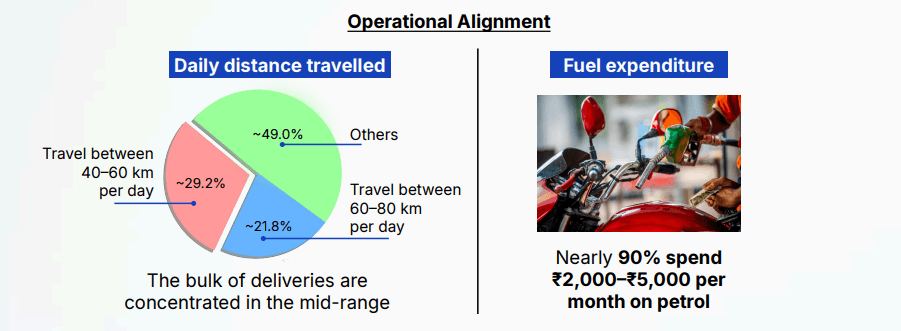

These operating patterns fall well within the real-world performance range of electric two-wheelers currently available in India, even under stop-start delivery conditions (NITI Aayog, 2025)

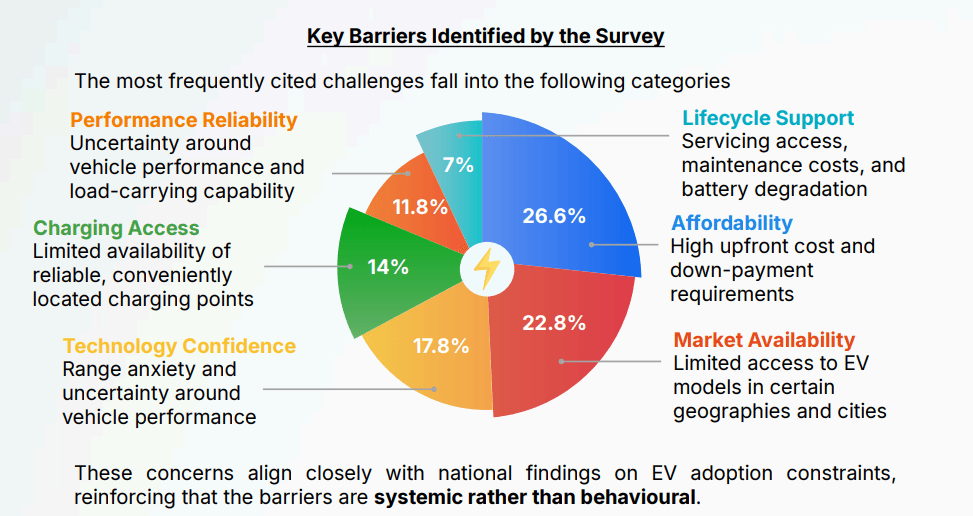

This intent–action gap indicates that reluctance is not ideological. Instead, delivery partners consistently cited practical, livelihood-related concerns.

4) National Signals: Policy and Fiscal Alignment

National policy signals increasingly reinforce the strategic importance of last-mile electrification within Indiaʼs broader electric mobility and industrial growth agenda. The Union Budget 2026–27 marked a clear evolution in approach - moving beyond consumer subsidies toward structural investments that strengthen the EV ecosystem.

The Budget underscored this shift through four key signals:

• Ecosystem-first policy orientation: The Budget prioritised battery manufacturing competitiveness, supply-chain resilience, and long-term cost reduction over consumption-led incentives, signalling the importance of deeper ecosystem readiness in driving sustained EV adoption.

• Continued support through PM E-Drive: The ₹1,500 crore allocation to the PM Electric Drive Revolution in Innovative Vehicle Enhancement (PM E-Drive) reaffirmed the commitment to advancing the commercial and last-mile EV segments, including two- and three-wheelers, buses, and trucks, alongside charging infrastructure.

• Battery value-chain and cost reduction measures: Customs-duty exemptions on capital goods and critical battery inputs, lowering domestic cell and battery production costs.

• Localisation and supply-chain resilience: Targeted support for domestic EV and auto-component manufacturing, including MSME participation, reinforced EV adoption as an industrial and climate strategy, and not a standalone transport intervention.

Together, these measures align EV adoption with Indiaʼs manufacturing, energy-security, and climate objectives.

Fiscal Rationale for Prioritising the Last Mile

From a fiscal and climate-efficiency perspective, the Budgetʼs ecosystem-led approach complements evidence that electric two-wheelers deliver significantly higher CO₂ abatement per rupee of government support than electric passenger cars, driven by lower upfront costs and substantially higher utilisation rates in delivery use cases (CSEP, 2026).

In summary:

• Usage intensity matters more than vehicle class in determining near-term emissions benefits.

• High-utilisation last-mile fleets therefore represent one of the most efficient climate investments available today.

• Long-term ecosystem support, across manufacturing, components, charging, and finance, reduces lifecycle costs and improves risk-adjusted returns for operators.

Taken together, the Union Budget 2026 and ongoing national priorities position last-mile electrification as a central pillar of Indiaʼs EV strategy, requiring calibrated fiscal support and sustained ecosystem development to unlock scalable adoption.

5) The Enabling Ecosystem: What Works at Scale

Evidence from India and global markets suggests that last-mile electrification scales only when multiple ecosystem levers move together.

1. Financing Innovation

National consultations recommend shifting from high upfront capital expenditure to leasing, low-cost loans, and battery-as-a-service models, particularly for small operators (NITI Aayog, 2025).

2. Charging-as-a-Service

Globally, EV charging is increasingly delivered as a managed service rather than owned infrastructure. The EV Charging-as-a-Service market is projected to grow from USD 2.6 billion in 2026 to USD 16.8 billion by 2036, driven largely by fleet and commercial demand (Future Market Insights, 2026). This model aligns well with hub-based last-mile delivery operations.

3. Fit-for-Purpose Vehicles

Delivery-optimised EVs - designed for payload, durability, and urban duty cycles - reduce performance anxiety and downtime (CII & Clean Air Fund, 2025).

4. Training and Awareness

Structured onboarding and training are critical to addressing misconceptions around EV safety, range, and maintenance, a gap national consultations have repeatedly highlighted (NITI Aayog, 2025).

5. Lifecycle Assurance

Servicing networks, structured buy-back mechanisms, and emerging battery passport systems - digital records that track battery health, usage, and lifecycle history, reduce long-term risk for drivers and financiers alike (NITI Aayog, 2025).

6) Impact Potential of Last-Mile Electrification

Electrifying last-mile delivery fleets has the potential to generate compound benefits across economic, environmental, operational, and systemic dimensions. Unlike private vehicle electrification, which often depends on lifestyle change and long asset-replacement cycles, last-mile fleets operate as high-utilisation economic assets, allowing benefits to accrue rapidly and predictably.

6.1 Economic Impact: Income Stability and Cost Reduction

For delivery partners, vehicle choice is a livelihood decision. Fuel and maintenance costs represent one of the largest recurring expenses, directly affecting take-home income.

Evidence from industry studies indicates that:

• Electric two- and three-wheelers can reduce fuel and energy costs by 70–80% compared to petrol vehicles in last-mile use cases

• Lower maintenance requirements further reduce operating costs, resulting in 15%–20% potential net income uplift for delivery partners operating EVs at scale (CII & Clean Air Fund, 2025)

Survey data reinforces this potential. Nearly 90% of delivery partners currently spend ₹2,000–₹5,000 per month on petrol, indicating substantial room for savings when supported by appropriate financing and charging access. Importantly, these gains are recurring, improving income resilience rather than offering one-time benefits.

From a systemic perspective, improved earnings also:

• Reduce delivery-partner churn

• Improve workforce stability

• Lower recruitment and onboarding costs for logistics platforms.

6.2 Environmental Impact: Air Quality and Climate Benefits

Climate outcomes from electrification are shaped less by vehicle category and more by how intensively vehicles are used, positioning electric two-wheelers as a particularly effective decarbonisation lever in delivery applications (CSEP, 2026).

Last-mile delivery vehicles disproportionately contribute to urban air pollution due to their operation in dense, high-exposure environments. Tailpipe emissions of PM2.5 and NOx from two-wheelers are strongly associated with respiratory and cardiovascular health impacts in Indian cities (CII & Clean Air Fund, 2025).

Full electrification of urban last-mile delivery fleets has been estimated to:

• Eliminate thousands of tonnes of PM2.5 emissions annually

• Reduce NOx emissions at scale, particularly in non-attainment cities (CII & Clean Air

Fund, 2025)

In Indiaʼs current grid context, where electricity still has a relatively high emissions factor, usage intensity is the dominant determinant of climate benefit. Electrifying vehicles that travel more kilometres per day therefore delivers greater near-term emissions reductions than electrifying lightly used private cars.

6.3 Operational Impact: Predictability and Resilience

Electrification also improves operational resilience for delivery ecosystems.

EVs reduce exposure to:

• Fuel price volatility, which directly affects delivery economics

• Supply disruptions linked to petrol availability

At the fleet level, predictable charging schedules and lower mechanical complexity enable:

• Better route planning

• Reduced downtime

• More consistent delivery performance

Charging-as-a-service models, particularly hub-based charging near logistics facilities, further enhance predictability by shifting infrastructure management away from individual drivers (Future Market Insights, 2026).

6.4 Systemic Impact: Scaling Inclusive Electrification

Perhaps the most significant impact of last-mile electrification lies in its systemic impact. Indiaʼs transport sector is highly fragmented, characterised by millions of small vehicle owners, independent delivery partners, and micro-entrepreneurs operating at the frontlines of urban logistics. Successfully electrifying last-mile delivery shows that:

• EV adoption is feasible even without consolidated, corporate fleet ownership

• Small operators can transition to EVs when financial and operational risk is reduced

• Clean mobility can scale inclusively, without concentrating benefits in a narrow set of large players

In doing so, last-mile electrification challenges the assumption that electric mobility can advance only through large fleets or capital-intensive ownership models. Instead, it demonstrates a pathway to broad-based, equitable adoption.

At full scale, last-mile delivery represents one of Indiaʼs largest private-sector EV transitions, with implications for:

• Urban air-quality management

• Energy demand planning

• Workforce skilling and job creation

• Investor confidence in Indiaʼs EV ecosystem

7) Conclusion

Indiaʼs electric mobility transition is often framed as a question of technology readiness or consumer willingness. Evidence from delivery partners, national policy analysis, and industry research add more perspective.

The technology already exists. The willingness already exists. What remains is the alignment of systems.

The findings presented in this whitepaper unequivocally prove that:

Resistance to EV adoption in last-mile delivery is not a matter of mindset, but is contingent on infrastructure, finance, and risk factors.

Delivery partners operate within narrow economic margins. Their vehicle decisions are shaped by:

• Upfront affordability

• Predictability of daily operations

• Assurance of servicing and resale value

Where risk-reduction mechanisms are missing, adoption plateaus, even when the business case is strong. Where financing, infrastructure, and operational assurance converge, electrification scales swiftly, as evidenced in early city-level clusters.

Making Last-Mile Electrification a National Priority

National policy direction reinforces a clear conclusion: India will not meet its 30% EV penetration target by 2030 through incentives alone (NITI Aayog, 2025). The next phase of electric mobility growth must move beyond broad-based subsidies toward targeted, systems-level acceleration.

For policymakers and regulators, this means three priorities:

• Target high-utilisation segments first, especially last-mile delivery fleets, where emissions reductions per vehicle are significantly higher due to daily usage intensity.

• Shift from asset subsidies to ecosystem enablement, including low-cost financing, charging-as-a-service models, battery lifecycle transparency, and structured buy-back mechanisms that reduce adoption risk.

• Strengthen coordination across logistics players, OEMs, financiers, energy providers, and urban authorities to ensure infrastructure deployment, vehicle design, and financing evolve in alignment.

From a fiscal and climate standpoint, this focus is not only strategic but efficient. Electric two-wheelers in delivery use cases generate higher emissions abatement per rupee of public support than most other vehicle categories (CSEP, 2026). Prioritising last-mile electrification, therefore, maximises near-term climate returns while minimising fiscal strain.

Equally important, this transition is fundamentally people-centred. Indiaʼs transport ecosystem is characterised by fragmented ownership and small operators. By reducing financial and operational risk for delivery partners and small fleet owners, last-mile electrification demonstrates that climate action and income stability can advance together.

The last mile is therefore more than an operational segment. It is a strategic proof point:

• That clean mobility can scale inclusively

• That electrification can succeed beyond large consolidated fleets

• That climate action can be embedded in everyday economic activity

Indiaʼs electric mobility future will not be defined solely by private cars or long-haul trucking corridors. It will be shaped in dense urban streets, through high-frequency delivery routes, and through the cumulative impact of thousands of small operators transitioning with confidence.

If India is to accelerate its EV transition meaningfully this decade, last-mile electrification must be treated not as a niche initiative, but as a central pillar of national mobility strategy.

8) Methodology & Scope

Research Design: A Mixed-Method Approach

This whitepaper is grounded in a mixed-method research design, combining:

• Primary research through a structured survey of delivery partners (“Wishmastersˮ) across India

• Secondary research drawn from national EV policy documents, fiscal assessments, and industry reports

This integrated approach ensures that findings reflect both frontline operational realities and broader ecosystem, fiscal, and regulatory dynamics shaping Indiaʼs EV transition.

Primary Research: Delivery Partner Survey

Research Objective: In alignment with the organisationʼs EV100 commitment and the scale of its delivery workforce across India, the survey was designed to:

• Assess willingness to transition to EVs

• Understand operational metrics (daily mileage, fuel expenditure, vehicle ownership)

• Identify primary blockers to EV adoption

• Inform ecosystem interventions, including financing and charging partnerships

The survey aimed to generate actionable insights that directly inform programme design, particularly in areas such as infrastructure partnerships and access to credit through internal NBFC mechanisms.

Survey Instrument

The questionnaire captured data across four categories:

1. Operational Metrics

• Average daily distance travelled

• Monthly fuel expenditure

• Number of operating days per month

• Vehicle ownership model

2. EV Adoption Intent

• Willingness to switch to EV

• Perceived benefits

• Awareness of total cost of ownership

3. Barriers to Adoption

• Upfront cost and down payment constraints

• Financing access

• Charging availability

• Range and performance concerns

• Servicing and other lifecycle concerns

4. Required Enablers

• Preferred financing structures

• Charging preferences (home vs hub-based vs public)

• Ecosystem support required

• Awareness

Data collection was conducted via Disperz App: Enterprise Learning app betweenmAugust 2025 and January 2026

Secondary Research Integration

Survey findings were contextualised using secondary research from:

• National EV policy diagnostics

• Fiscal efficiency analyses

• Industry research on zero-emission delivery

• Charging infrastructure and EV ecosystem assessments

Secondary sources were used to:

• Validate systemic barriers identified in the survey

• Benchmark climate-efficiency insights

• Align regional findings with policy signals

• Assess infrastructure-readiness patterns

This ensured that frontline insights were interpreted within Indiaʼs broader EV transition framework rather than treated in isolation.

Limitations

• Participation may reflect self-selection bias

• Willingness does not automatically translate to adoption without enabling conditions

• Regional willingness data does not fully capture infrastructure density differences

• Information collected for the secondary research is from public domains, and Flipkart will not be responsible for any errors in the same.